Unlike many developed nations, the beauty of the Indian economy lies in its ability to rebound very quickly, irrespective of the political dispensation in power. Therefore, before the Modi government rushes to celebrate the International Monetary Fund’s (IMF) latest projection, it would do well to recall how India survived the 2008 global financial crisis under the Congress-led government.

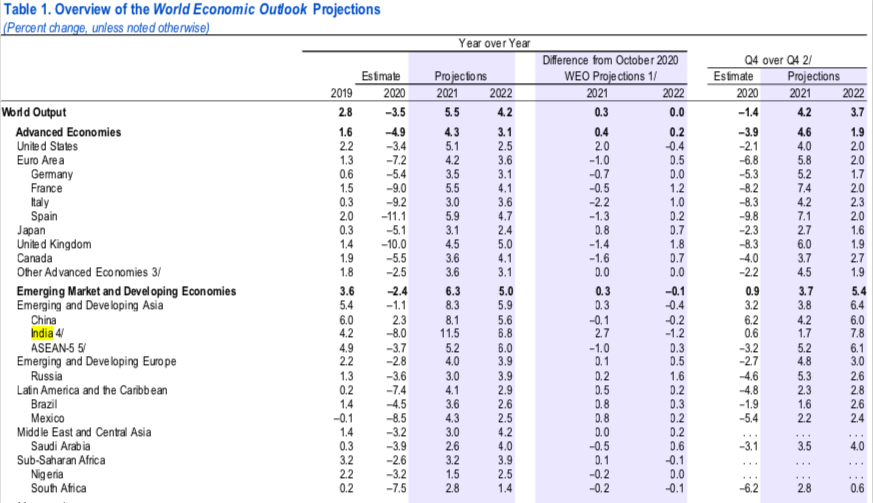

The IMF on Tuesday came out with the 2021 projection for the world economy, predicting double-digit growth for India, at 11.5%. It said India would be the lone major economy to register this growth, outpacing nations such as China, Spain, and France. It reflects a strong rebound in the Indian economy battered by the Covid-19 pandemic, especially when the rest of the world is yet to come out of a deep recession.

The IMF’s latest World Economic Outlook shows China would grow at 8.1%, followed by Spain (5.9%) and France (5.5%). The latest projections once again put India among the fastest developing economies of the world.

This would surely enthuse the ruling Bharatiya Janata Party (BJP), which has drawn flak from multiple quarters for its inability to handle domestic crises such as the initial phase of the pandemic, the massive job losses on account of months-long lockdown, problems faced by the country’s farmers among others. And what the government has done to mitigate some of these crises is far from satisfactory.

For the record, India’s economy contracted 8% in 2020, according to IMF. China is the only major economy to have seen a positive growth rate of 2.3% last year. In India, 122 million people were estimated to have lost jobs in April 2020 because of the nationwide lockdown, according to the Centre for the Monitoring of the Indian Economy (CMIE), a leading business information company. More than three-fourths of these were wage laborers and small traders.

However, there had been a steady decline in this trend until August when the net loss was pegged at 11 million. “Much of what could be recovered quickly has been so. The remaining recovery could be a long haul,” Mahesh Vyas, MD and CEO, CMIE told Indian news magazine, The Week, in September 2020.

Perhaps the New Year has ushered in a hope of better days ahead as the economy starts showing signs of recovery, thanks to the decreasing trend of the Covid-19 and the nationwide rollout of the vaccines. Financial news agency Bloomberg says, while the consumer confidence and the demand are likely to grow further, the government could infuse fresh stimulus in the upcoming Union Budget.

The 2008 Global Financial Crisis

The 2008 global financial crisis that had its epicenter in the US is considered the worst economic disaster since the Great Depression of 1929. The knockout punch, if one may like to call it, came when America’s fourth-largest investment bank Lehman Brothers had gone bust on September 15, 2008.

And the ripple effects were felt globally as equity markets had lost $10 trillion in their market capitalization. It triggered a worldwide banking crisis owing to the low confidence in the banks. But India somehow managed to escape with minor bruises.

Despite the global recession, India’s economy grew at the rate of 6.7% in the 2008-09 fiscal year mainly because India’s exports account for only 15% of the Gross Domestic Product (GDP), less than half the levels of major Asian economic powers such as China and Japan, according to the financial magazine Forbes.

While the rest of the world was recovering from the upheaval, India remained the second-fastest growing economy of the world, eminent author and lawmaker Shashi Tharoor wrote in a piece for Project Syndicate.

The recession coincided with the 2008 terror attacks in Mumbai, India’s financial capital, in which 166 people, including several foreign nationals, were killed. India and the US have blamed Pakistani terrorists and elements within the Pakistani security establishment for this dastardly act.

“The terrorists dented the worldwide image of India as an emerging economic giant, a success story of the era of globalization, and a magnet for investors and tourists,” Tharoor wrote.

He also noted that foreign investors had withdrawn $12 billion from India’s share market. “But India’s resilience in the face of adversity and its mature restraint in the face of violent provocation encouraged investors to return.

“Foreign direct investment totaled $27.3 billion in 2008-2009 despite the global financial crisis and reached $1 billion in just one week….” Tharoor, a senior leader of the Congress party, added.

State of The Economy

The IMF’s latest projection once again proves that India would be able to recover from the pandemic-inflicted injuries much faster than many developed countries, according to experts.

Speaking to The Eurasian Times, Dr. Rouhin Deb, an independent economist and researcher, says,

“The projected 11.5 % growth figures by IMF for India are testimony to the inherent resilience and fighting spirit of 130 crore Indians.

“Right policy interventions during the pandemic across various champion sectors, besides measures such production-linked incentives (for the manufacturing sector), labor codes reforms, calibrated use of resources in the entire Covid period are primary reasons for the strong global confidence in the India story.

“In these times when the whole world witnessed negative FDI growth rates, India stood its ground with one of the best FDI growth rates in the world. The clarion call for ‘Atmanirbhar Bharat’ and ‘Make in India’ seems to have struck the right chord with the masses and the world has acknowledged India’s prowess to bounce back from the worst of the setbacks.”